Smiths Group announced that it has entered into an agreement for the proposed sale of Smiths Detection to funds advised by CVC Capital Partners. The proposed transaction values Smiths Detection at an enterprise value of £2.0bn, representing 16.3x headline operating profit of £122m and 12.5x headline EBITDA of £160m for the financial year ending 31 July 2025. Based on customary adjustments, Smiths expects to receive net cash proceeds of approximately £1.85bn.

The proposed transaction, in combination with the recently announced sale of Smiths Interconnect, represents significant further progress on the strategic actions announced in January 2025. This repositions Smiths as a focused, high-performance, industrial engineering company and delivers significant value for all stakeholders.

Subject to completion of information and consultation processes with the works council of Smiths Detection France SAS, and customary regulatory approvals, completion of the proposed transaction is expected in the second half of calendar year 2026.

“Today we have reached another significant milestone for Smiths, with the agreement to sell Smiths Detection to CVC for an enterprise value of £2.0bn,” said Roland Carter, chief executive of Smiths. “This builds on our recently announced sale of Smiths Interconnect and demonstrates strong execution against the strategic actions we set out in January centered on value creation. We are focusing Smiths as a premium industrial engineering company specializing in flow management and thermal solutions, and today’s announcement positions us strongly to deliver enhanced growth and returns. We thank our Smiths Detection colleagues for their significant contribution to Smiths and their help in reaching this milestone.”

Proposed Transaction highlights

- Highly attractive valuation: the enterprise value of £2.0bn represents a multiple of 16.3x headline operating profit of £122m and 12.5x headline EBITDA of £160m for the financial year ending 31 July 2025.

- The Proposed Transaction, together with the sale of Smiths Interconnect announced in October 2025, represents a combined enterprise value of £3.3bn.

- With the Proposed Transaction and the agreed sale of Smiths Interconnect, Smiths is now in the process of executing both strategic portfolio actions announced in January. Together, these transactions demonstrate continued progress in delivering on actions designed to maximize value creation, unlock portfolio value and enhance returns to shareholders.

- Repositions Smiths as a high-performance industrial engineering company focused on technologies in flow management and thermal solutions with high customer-centricity, leading positions in attractive, growing segments and a strong financial profile.

- Smiths intends to return a large portion of the net cash proceeds from the Proposed Transaction to shareholders and will provide an update on timing and mechanism in due course.

- Smiths intends to maintain a strong and efficient balance sheet alongside a solid investment-grade credit rating, whilst executing the £1bn buyback announced on 19 November 2025.

- Completion is expected in the second half of calendar year 2026, subject to the Consultation and customary regulatory approvals.

Proposed Transaction background and rationale

As announced on 31 January 2025, Smiths is committed to a strategy designed to unlock significant value, enhance returns to shareholders and deliver above market growth over the medium term.

A core element of this strategy is to focus Smiths as a high-performance industrial engineering company. Smiths supports customers in attractive energy, industrial and construction end markets underpinned by structural megatrends, and is well positioned for continued growth and margin expansion.

To achieve this, Smiths announced plans to separate both Smiths Detection and Smiths Interconnect in January 2025. The sale of Smiths Interconnect to Molex Electronic Technologies Holdings, was announced on 16 October 2025. With the proposed transaction, Smiths is now in the process of executing both major portfolio actions outlined in the January strategic update.

After a competitive sale process, the Smiths Board of Directors concluded that the terms of the Proposed Transaction represented a compelling value proposition, and a more compelling outcome than the alternative demerger which was also under consideration. In particular, the Smiths Board believes that:

- The Proposed Transaction value fully reflects the long-term growth and margin expansion prospects of Smiths Detection.

- The Proposed Transaction value compares strongly against relevant publicly available benchmarks.

- The immediate realization of cash is a preferred outcome for shareholders, as compared to the demerger proposal.

- The net cash proceeds support further growth, as well as further substantial capital returns to shareholders over the medium term and provide an opportunity to invest in a more focused Smiths.

A new Smiths focused on efficient flow management and thermal solutions

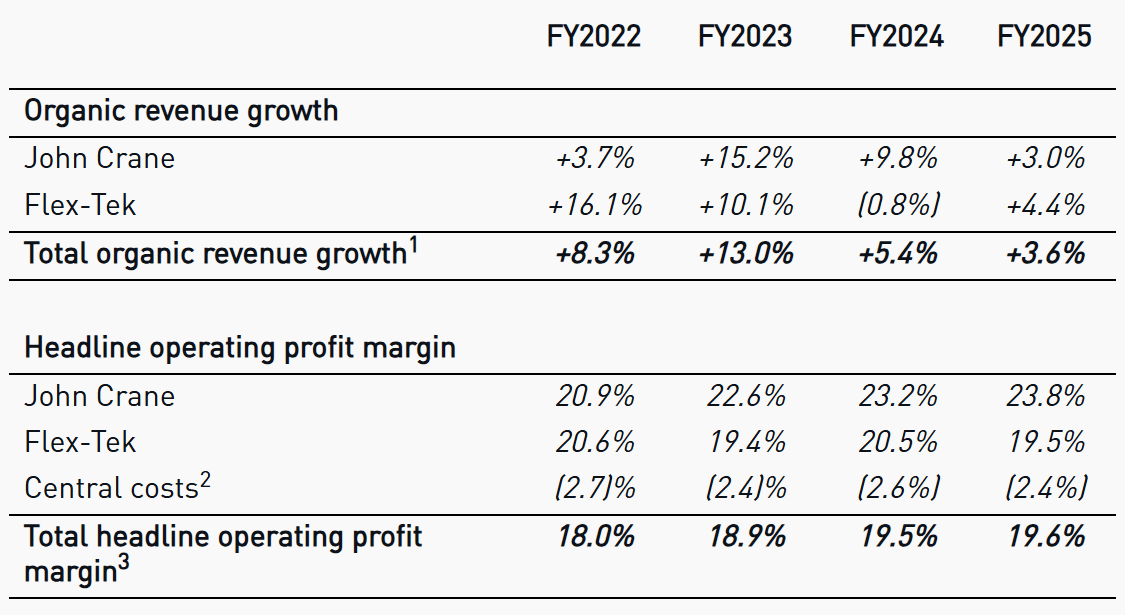

The strategic actions taken position Smiths as a focused, stronger business specializing in efficient flow management and thermal solutions. Smiths, following Completion and completion of the sale of Smiths Interconnect, will have a stronger financial profile and growth potential, with the table below showing the historical financial performance of the combined John Crane and Flex-Tek businesses:

In March 2025, Smiths set out its new enhanced medium-term financial targets that reflect this superior financial potential of Continuing Smiths following Completion:

- Growth focused: 5-7% organic revenue growth through-cycle, with a

21-23% headline operating profit margin and headline EPS growth of more than 10%. - Cash generative: ~100% operating cash conversion, with a ROCE above 20%.

- Disciplined allocators of capital: Smiths will drive growth and productivity through RD&E, operational excellence and value-accretive acquisitions, underpinning a progressive dividend and enhanced returns to shareholders.

The Acceleration Plan to deliver productivity and capability enhancements, and a streamlined cost base, will help support the achievement of these targets. Smiths remains on track to deliver £40-45m annualised benefits in FY2027 and beyond, with approximately half expected in FY2026, for a total cost of £60-65m. Around 2/3 relates to the retained businesses and targets central costs remaining at 1.5-1.7% of revenue, following completion of the separation processes.